Unit Economics 101: The 6 Numbers Investors Stress-Test in Indian Startups (2026)

I have sat on the founder’s side of enough fundraising conversations to know the exact moment a pitch changes gear. It is not when the founder shows the hockey-stick revenue chart. It is the question that comes right after: “What does one customer actually cost you, and what do they actually make you?”

That single question is unit economics. And in 2026, after two hard years of funding discipline, it is the part of your numbers that decides whether an investor leans in or quietly starts looking for the exit.

This guide breaks down the six unit economics numbers that investors stress-test in Indian startups, why each one matters, the specific trap Indian founders fall into on each, and what a healthy number actually looks like. None of this is accounting jargon. It is the language investors use to decide if your growth is real.

Key Takeaways

- Investors do not fund revenue growth. They fund a business where each customer makes more money than it costs to win and serve. Unit economics is how they check that.

- Six numbers carry almost all the weight in an early Indian round: gross margin, contribution margin, CAC payback period, LTV to CAC ratio, net revenue retention, and burn multiple.

- The most common Indian trap is reporting GMV or top-line growth while the real per-order economics stay negative once payment-gateway, logistics, discount and support costs are loaded in.

- A startup that grows fast on negative unit economics is not a rocket. It is a subsidy. Investors learned to spot the difference after the 2022 to 2024 funding reset, and the burn multiple is now a standard lens.

- You should be able to produce all six numbers, with the calculation behind each, before an investor asks. If you cannot, that is the gap to close first.

What Unit Economics Actually Means

Unit economics is the profit and loss of a single unit of your business, usually one customer or one order, stripped of all the company-level noise. It answers one question: if you do this one more time, do you make money or lose money?

A company can be growing revenue 200 percent a year and still have broken unit economics. That is the case investors fear most, because scaling a money-losing unit just loses money faster. Strong unit economics is the opposite signal: it tells an investor that capital poured into growth comes back multiplied, not burned.

Here are the six numbers, in the order an investor usually works through them.

1. Gross Margin: Is the Core Business Even Profitable?

Gross margin is revenue minus the direct cost of delivering your product or service, expressed as a percentage. For a software product, that is hosting, payment fees and direct support. For a commerce or services business, it includes procurement, fulfilment and delivery cost.

Why investors test it: Gross margin sets the ceiling on everything else. A business with 70 percent gross margin can afford to spend on growth and still keep most of each rupee. A business at 15 percent margin cannot, no matter how fast it grows.

The Indian trap: Services revenue dressed up as software. A founder pitches a “SaaS” multiple but the margins look like a services company because half the revenue needs human delivery. Investors find this in minutes by dividing gross profit by revenue. If your “software” business runs at 35 percent gross margin, the story and the numbers do not agree, and the numbers win.

What good looks like: 70 percent and above for pure software. 30 to 50 percent for commerce and marketplaces depending on category. 50 percent and above for tech-enabled services. The exact number matters less than whether you can explain it honestly.

2. Contribution Margin: Does One Order Make Money After Everything Variable?

Contribution margin goes one level deeper than gross margin. It is what is left from one sale after every cost that varies with that sale: cost of goods, payment-gateway charges, shipping, packaging, cashback, the support time that order consumes. What remains contributes to your fixed costs and eventually to profit.

Why investors test it: This is the truest test of whether your business model works at the level of a single transaction. A positive contribution margin means more volume eventually leads to profit. A negative one means more volume leads to a bigger hole.

The Indian trap: The discount and cashback that never shows up in the headline. Many Indian consumer startups quote gross order value while quietly funding a 20 to 30 percent effective discount through coupons, free delivery and cashback. Load those back in and a “profitable” order is underwater. Investors rebuild this number from the cash that actually left your account, not from the price on the invoice.

What good looks like: Positive and improving with scale. Even a thin positive contribution margin that is trending up tells a far better story than a fat gross margin sitting on top of a negative contribution margin.

3. CAC Payback Period: How Long Until a Customer Pays You Back?

Customer Acquisition Cost, or CAC, is the fully loaded cost of winning one customer: ad spend, sales salaries, commissions and the tools that support them, divided by the customers won. CAC payback period is how many months of that customer’s gross profit it takes to earn the CAC back.

Why investors test it: Payback period is a cash-flow truth-teller. A short payback means your growth largely self-funds. A long payback means every new customer needs working capital to carry for months, and that is exactly the capital the investor is being asked to supply.

The Indian trap: Blended CAC that hides the paid number. Founders average their cheap organic and referral customers in with expensive paid ones to produce a flattering “blended CAC”. Investors ask for the paid CAC alone, because that is the number that scales when you put their money into acquisition. If blended CAC is Rs 400 and paid CAC is Rs 2,200, only the second one matters at scale.

What good looks like: Under 12 months for most models, under 6 months is strong, and 18-plus months needs a very high retention story to justify it.

4. LTV to CAC Ratio: For Every Rupee Spent Winning a Customer, How Many Come Back?

Lifetime Value, or LTV, is the total gross profit you expect from a customer across the whole relationship. The LTV to CAC ratio compares that to what you spent to acquire them. It is the headline efficiency number of the whole acquisition engine.

Why investors test it: It tells them whether your growth spend creates value or destroys it. A ratio of 3 to 1 means each rupee of acquisition returns three rupees of lifetime gross profit. Below 1 to 1, you are paying customers to leave.

The Indian trap: An LTV built on a retention curve you do not have yet. Early founders project a five-year customer life from three months of data and an optimistic churn assumption. Investors discount LTV claims that are not backed by real cohort retention. The fix is to show actual retention by monthly cohort, not a single assumed number.

What good looks like: 3 to 1 is the classic benchmark. Above 3 with a short payback is excellent. Below 3, or a healthy ratio built only on a long projected lifetime, will draw hard questions.

5. Net Revenue Retention: Does Your Existing Base Grow or Leak?

Net Revenue Retention, or NRR, measures how revenue from a cohort of existing customers changes over a year, including upgrades, downgrades and churn, before any new customers are added. An NRR of 110 percent means last year’s customers are worth 10 percent more this year even if you signed nobody new.

Why investors test it: NRR is the closest thing to a structural growth engine. High NRR means the business compounds on its own base and new sales sit on top of a rising floor. Low NRR means you are refilling a leaking bucket and growth is entirely dependent on ever-rising acquisition spend.

The Indian trap: Counting logo retention instead of revenue retention. A founder proudly reports that 90 percent of customers stay, while ignoring that the average customer downgraded their plan. Logos can stay while revenue shrinks. Investors want the revenue number, not the headcount number.

What good looks like: 100 percent and above is the line where the base is self-sustaining. 110 percent and above for SaaS is strong. For transactional consumer businesses, repeat-purchase rate and cohort revenue retention are the equivalent signals.

6. Burn Multiple: How Much Cash Do You Burn for Each Rupee of New Revenue?

Burn multiple is net cash burned in a period divided by net new annual recurring revenue, or net new revenue, added in that same period. It became the defining metric of the post-2022 funding environment because it captures growth efficiency in a single number.

Why investors test it: It answers the question that matters most after the easy-money years: how much are you spending to buy growth? A burn multiple of 1 means you burned one rupee to add one rupee of new revenue. A burn multiple of 4 means you burned four rupees for the same result, which is the profile that stopped getting funded.

The Indian trap: Treating a high burn multiple as ambition rather than inefficiency. Before 2022, heavy burn signalled aggression and investors rewarded it. That era is over. In 2026, a high burn multiple with no clear path to improving it reads as a business that does not yet work, not one that is growing boldly.

What good looks like: Under 1 is excellent, 1 to 2 is healthy, 2 to 3 is acceptable at early stage with a clear improvement path, and above 3 needs a very strong reason.

The 6 Numbers at a Glance

| Metric | What it answers | Healthy zone (early stage) |

|---|---|---|

| Gross margin | Is the core business profitable? | 70%+ SaaS, 30-50% commerce |

| Contribution margin | Does one order make money after all variable cost? | Positive and improving |

| CAC payback period | How fast does a customer repay acquisition cost? | Under 12 months |

| LTV to CAC | Return on each rupee of acquisition | 3 to 1 or better |

| Net revenue retention | Does the existing base grow or leak? | 100%+ (110%+ strong) |

| Burn multiple | Cash burned per rupee of new revenue | Under 2 |

How to Prepare These Before You Raise: A 5-Step Checklist

- Build one clean source of truth. Pull revenue, direct costs, acquisition spend and customer counts into a single model that you control, not five disconnected spreadsheets. Every number above must trace back to it.

- Load in the costs you are tempted to leave out. Payment-gateway fees, shipping, cashback, discounts, support time and your own salary. The numbers an investor rebuilds will include these, so yours should too.

- Show real cohort retention, not assumptions. Lay out monthly cohorts and let the retention curve speak. This is what gives your LTV and NRR credibility.

- Separate paid from blended. Report paid CAC and blended CAC side by side. Transparency here builds more trust than a single flattering figure.

- Know your improvement story for each number. Investors do not expect perfect unit economics at seed or Series A. They expect you to know exactly which number is weak and what specifically you will do to move it.

If you want to see how these metrics sit inside the wider picture investors examine, our 95-document due diligence checklist shows where financial readiness fits, and the startup cap table guide covers the equity side of the same conversation. For a structured view of how diligence-ready you are, the DD Readiness Score is a quick self-assessment.

Frequently Asked Questions

What is the single most important unit economics metric for an early Indian startup?

There is no single one, but if forced to choose, contribution margin is the foundation. If one transaction does not make money after every variable cost, no amount of scale or retention fixes the business. Investors often start there because everything else is built on it.

Do investors expect positive unit economics at seed stage?

Not always positive, but always understood. At seed, an investor accepts that some numbers are still developing. What they do not accept is a founder who cannot calculate them or does not know which one is broken. Knowing your weak number and your plan to fix it matters more than the number itself.

Why did the burn multiple become so important after 2022?

The funding reset of 2022 to 2024 ended the era where heavy burn signalled ambition. Capital became expensive and investors needed a single number that captured how efficiently a startup converted cash into durable revenue. The burn multiple does exactly that, which is why it is now a standard part of the conversation.

How is LTV to CAC different from CAC payback period?

CAC payback period is about time and cash flow: how many months until a customer repays their acquisition cost. LTV to CAC is about total return: how much lifetime gross profit a customer generates relative to that cost. A business can have a healthy LTV to CAC ratio but a long payback period, which still strains cash. Investors look at both together.

The Bottom Line

Unit economics is not a finance exercise you do for investors. It is how you find out whether the business you are building actually works. The six numbers above are simply the lens investors use to check the same thing you should already be tracking.

If you can produce all six, with the honest calculation behind each, before anyone asks, you have already separated yourself from most of the room. If you cannot yet, that gap is the most valuable thing to close before you start raising.

At A S Banka Advisors Private Limited, we help founders build investor-ready financial models and pressure-test their unit economics the way a diligence team will, before the diligence team does. If you are heading into a raise in the next two quarters, let’s discuss your situation: schedule a strategy session.

Disclaimer: This article is for general information only and does not constitute financial, legal or investment advice. Benchmark ranges are indicative and vary by sector, stage and business model. Please consult a qualified advisor for guidance specific to your company.

Related Posts

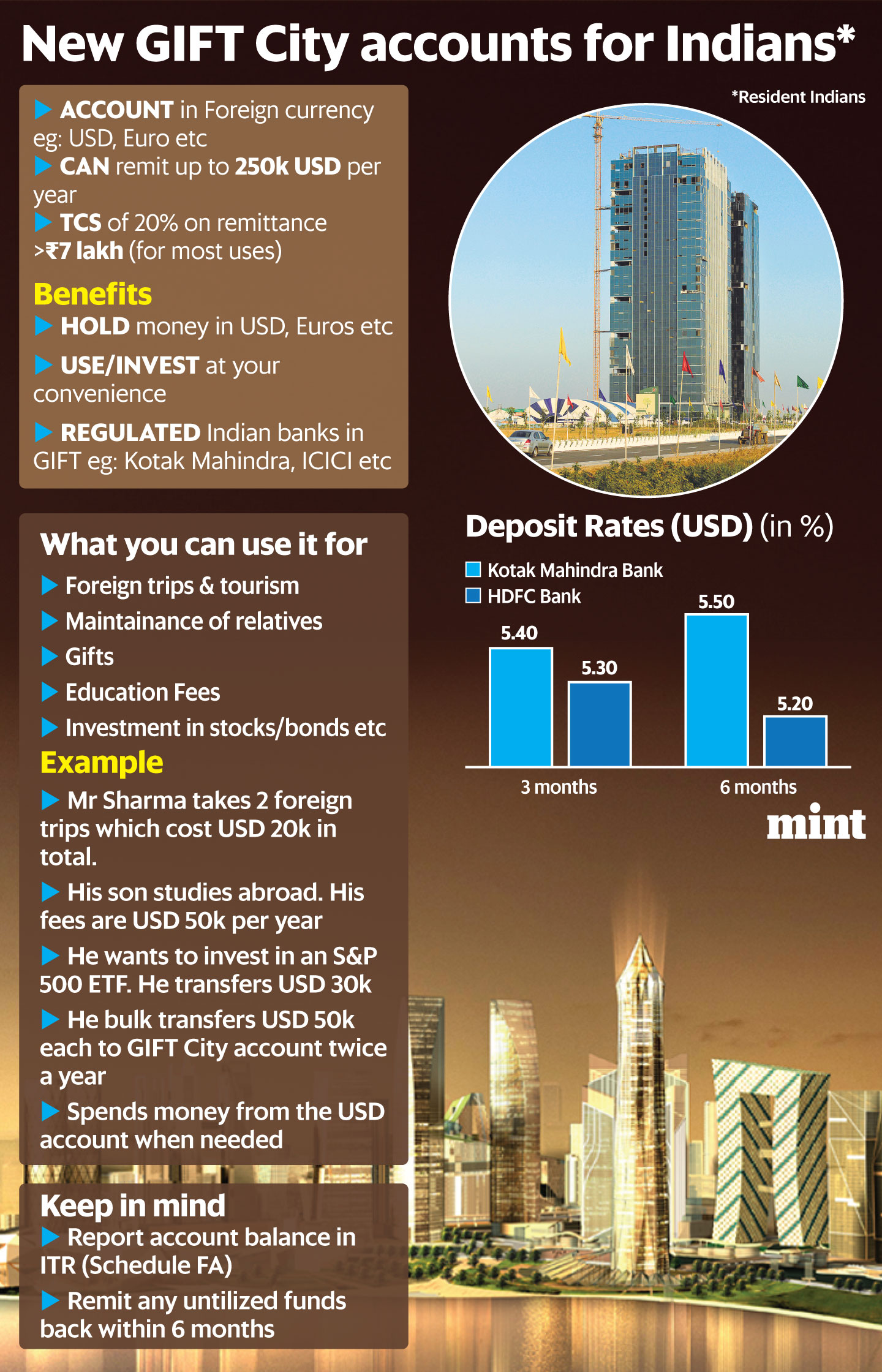

RBI allows Indian Resident to open foreign currency accounts in GIFT City under LRS

The new RBI circular allows an Indian Resident to open…

Game-Changer for Indian Exporters: Rs. 25,060 Crore Export Promotion Mission

Game-Changer for Indian Exporters: Rs. 25,060 Crore Export Promotion Mission…

The Startup Founder’s March 31 Compliance Checklist: 10 Deadlines You Cannot Miss

March 31 is the most consequential date on every Indian…