On June 19, 2026, the Securities and Exchange Board of India cleared one of the largest ease-of-doing-business packages the Alternative Investment Fund (AIF) industry has seen in years. The headline reform has an aviation-themed name: GARUDA, short for Green-channel: AIF Rollout Upon Document Acknowledgement. If you run an AIF, advise one, or are a founder raising from a domestic fund, the time it takes a new scheme to reach the market has just shrunk dramatically. Here is what it actually changes, and what you should do about it.

From “wait for the regulator” to “file, disclose, launch”

Under the old process, a manager launching a new scheme filed the private placement memorandum (PPM), usually through a merchant banker, and then waited for SEBI’s observations before accepting commitments. That review cycle could add weeks to the go-to-market timeline. Under GARUDA, an eligible scheme is treated as launched once SEBI acknowledges receipt of the documents. The regulator moves from a prior-approval posture to a disclosure-and-acknowledgement posture, with post-facto scrutiny replacing pre-launch gatekeeping. The reform is delivered through amendments to the SEBI (Alternative Investment Funds) Regulations, 2012 (Press Release No. 35/2026).

The new launch timelines depend entirely on your scheme bucket

- Accredited-investor-only schemes and angel funds: exempt from filing the PPM through a merchant banker; can launch immediately upon SEBI registration or filing of the PPM.

- Regular schemes (Category I / II / III): launch within 10 working days of filing under the GARUDA green-channel route.

- Large value funds (LVFs): continue under their existing accredited-investor framework.

The practical effect is significant. A manager who has built the portfolio thesis, lined up anchor commitments and got the documentation right can move from “filed” to “open for commitments” inside a fortnight for a regular scheme, and effectively on day one for an accredited-investor or angel structure. Classification is now the single most important decision: the wrong bucket means the wrong timeline and the wrong filing route.

The new AIF Master Circular: one document, 25 chapters

Running alongside the board reforms, SEBI issued a refreshed Master Circular for AIFs on June 3, 2026, updated June 16, consolidating every circular up to May 31, 2026 into a single 153-page, 25-chapter reference. Three provisions deserve specific attention: the Co-Investment Vehicle (CIV) framework (Chapter 6), which gives larger LPs a cleaner structure for deal-by-deal participation; the new Inoperative Fund status (Chapter 25), which lets a closed-portfolio AIF with pending tax or litigation matters retain proceeds and reduce compliance instead of a forced wind-up; and a streamlined quarterly activity report, with the first report under the new format reported as due July 15, 2026 for the quarter ending June 30, 2026. Confirm the exact date and format against the SEBI master circular and reporting portal before filing.

What this means for your fund, or your raise

For managers and sponsors, the speed is real, but so is the trade-off: with prior review compressed, the burden of getting disclosures, risk factors and conflict-of-interest statements right at the point of filing now sits squarely with you. For founders raising from AIFs, faster scheme launches and a smoother co-investment framework can translate into quicker cheque availability, particularly from angel and accredited-investor vehicles that back early-stage companies. For advisers, the work shifts upstream: the value is now in getting the PPM, valuation policy, fee structure and reporting right before filing, not in managing a review cycle afterwards.

Your four-step action plan

- Classify every planned scheme as accredited-investor-only, angel, regular, or LVF. The classification drives the timeline and the PPM route.

- Re-paper your PPM template to the disclosure standard a green-channel route demands, since SEBI now reviews post-facto.

- Map the GARUDA acknowledgement workflow so your team knows exactly what triggers the 10-working-day clock.

- Diarise the quarterly reporting cadence and review dormant schemes against the new Inoperative Fund status.

One caveat worth holding onto: the board approval is the policy; the implementing circular and amendment regulations are the mechanics. Watch for them before you rely on the exact contours. The fund that wins under GARUDA is the one whose documentation is launch-ready on the day it files, not the one hoping to fix things during review.

We have summarised the new launch buckets, the Master Circular provisions and the action plan in a detailed visual carousel. Download the full carousel PDF.

Structuring a launch-ready AIF, or raising from one? The classification and disclosure decisions you make now determine how fast you can move. Let’s discuss your situation. CA Adityavikram Banka, Founder, A S Banka Advisors Private Limited. Book a quick call: https://calendly.com/asbanka-info/30min

Related Posts

Eligibility Criteria for listing on SME Platform of BSE

New Eligibility Criteria for listing on SME Platform of BSE. …

Unit Economics 101: The 6 Numbers Investors Stress-Test in Indian Startups (2026)

Unit Economics 101: The 6 Numbers Investors Stress-Test in Indian…

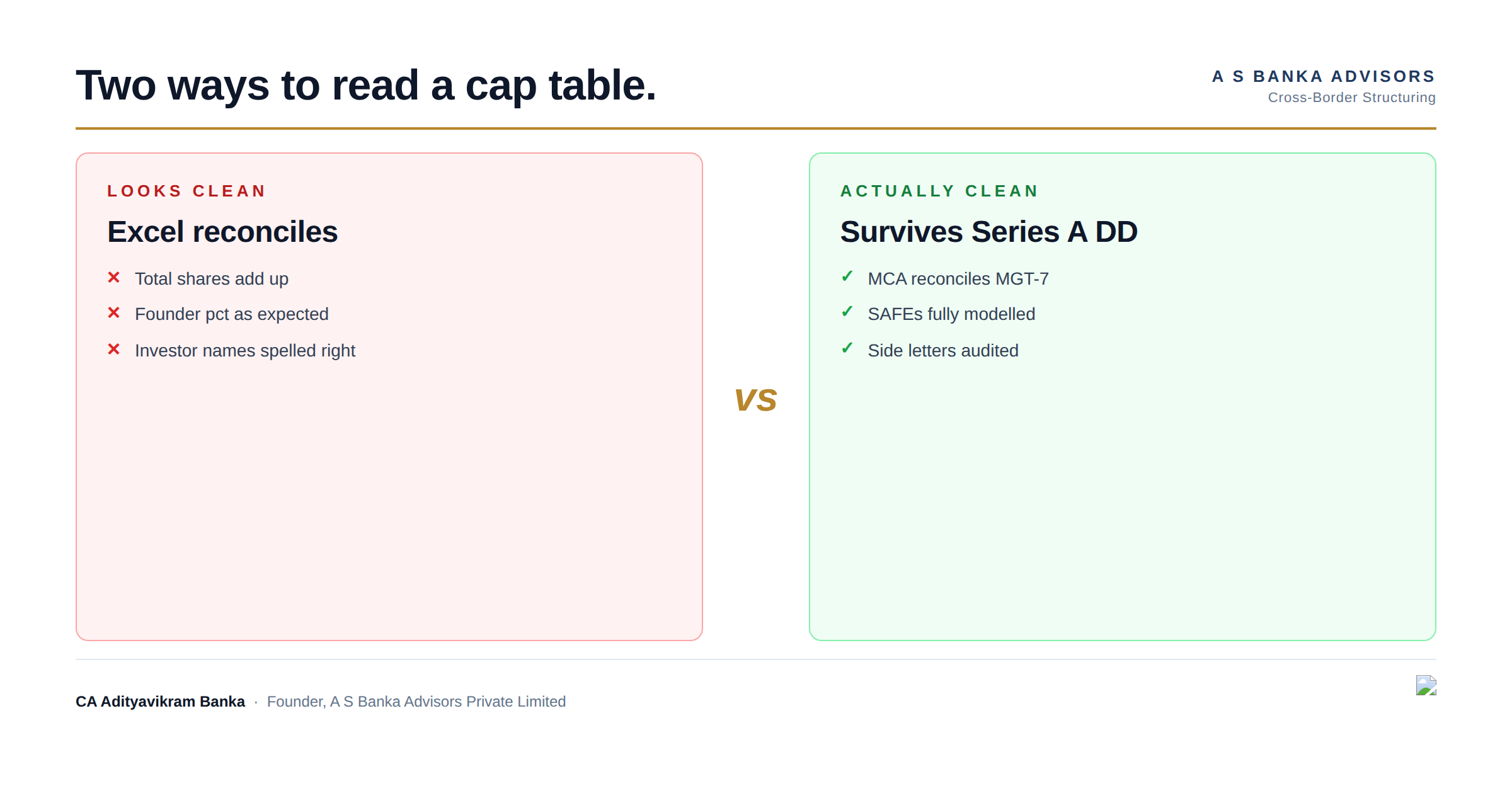

Why Your Cap Table Looks Clean But Isn’t

Key Takeaways A cap table that reconciles in Excel is…