The Landscape Has Shifted for Foreign Borrowing

If your startup or LLP has ever considered raising debt from overseas lenders, the rules just changed in your favour. The RBI’s new ECB framework, notified through FEMA 3(R)(5)/2026-RB on February 9, 2026, is the most significant overhaul of External Commercial Borrowing regulations in recent years. It is effective from February 16, 2026.

Here is what the five key changes actually mean for founders, CFOs, and their advisors.

1. Your Borrowing Headroom Just Got Bigger

The old annual ECB limit was a flat USD 750 million under the automatic route. The new framework raises this to the higher of USD 1 billion or 300% of your net worth (calculated on a standalone basis).

For a company with net worth of USD 500 million, that means borrowing capacity of up to USD 1.5 billion, double the old cap. Even for smaller companies, the 300% net worth formula means your borrowing headroom scales with your balance sheet strength.

2. LLPs Can Now Access ECBs Under the Automatic Route

This is a genuine game-changer for startups structured as LLPs. Previously, LLPs had to go through the approval route to access ECBs, which meant RBI scrutiny, processing delays, and uncertainty.

Under the new framework, LLPs are explicitly eligible under the automatic route. If you run a tech startup, consulting firm, or professional services business structured as an LLP, you now have a straightforward path to foreign debt capital without waiting for RBI approval.

3. Maturity Periods Are Now Predictable

The old framework had a confusing matrix of Minimum Average Maturity Periods (MAMP) ranging from 3 to 10 years depending on the end-use of funds. The new framework simplifies this to a clean 3-year standard MAMP for all ECBs.

Manufacturing companies get an additional advantage: a 1 to 3-year MAMP window capped at USD 150 million outstanding. This makes short-term foreign currency borrowing viable for equipment procurement and raw material financing.

4. Know What You Cannot Use ECB Funds For

For the first time, the RBI has codified the complete negative list in a single regulation: Regulation 3A. ECB proceeds cannot be used for chit funds, Nidhi company operations, agricultural activities, or TDR trading. Real estate is banned except for affordable housing and integrated townships. Securities market transactions are prohibited except for strategic M&A.

This is a practical improvement. Instead of checking multiple circulars, your compliance team now has one consolidated reference point.

5. Revised Reporting: Forms ECB 1 and ECB 2

All new ECB agreements from February 16, 2026 must use the revised Form ECB 1 (for registration and drawdown reporting) and Form ECB 2 (for monthly transaction reporting). Your AD Category I bank is responsible for verifying compliance before submitting to RBI.

What Should You Do Next?

If you have existing ECB agreements, review them for additional drawdown eligibility under the new limits. If you are an LLP, this is the right time to evaluate whether ECB makes sense for your growth capital needs. And regardless of structure, update your compliance processes to use the new forms and reference the codified negative list.

Download the full carousel PDF for a visual breakdown of all 5 changes.

Get Expert Guidance

Cross-border borrowing involves FEMA compliance, AD bank coordination, and careful end-use planning. If you need help structuring your ECB or evaluating whether the new framework works for your situation, book a quick call with A S Banka Advisors Private Limited.

Related Posts

3 distinct areas where founders are focusing in 2026

3 distinct areas where founders are focusing in 2026 :…

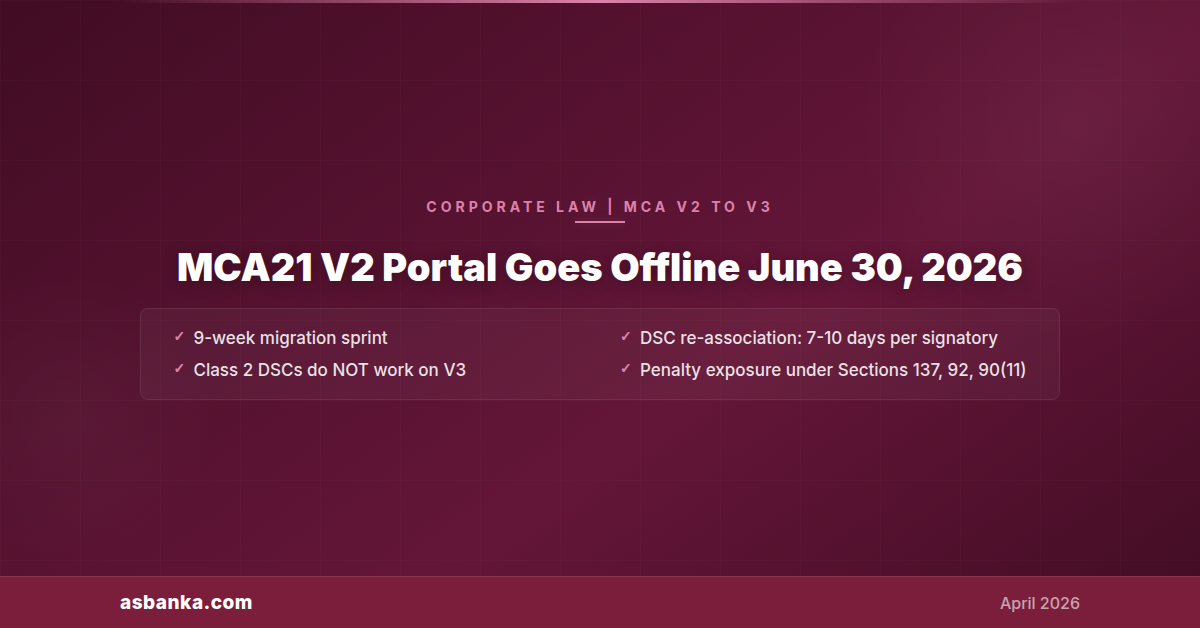

MCA21 V2 Portal Goes Offline June 30 2026: A 9-Week Migration Sprint for Indian Founders and Their Professionals

Most CA practices we have spoken to in the last…

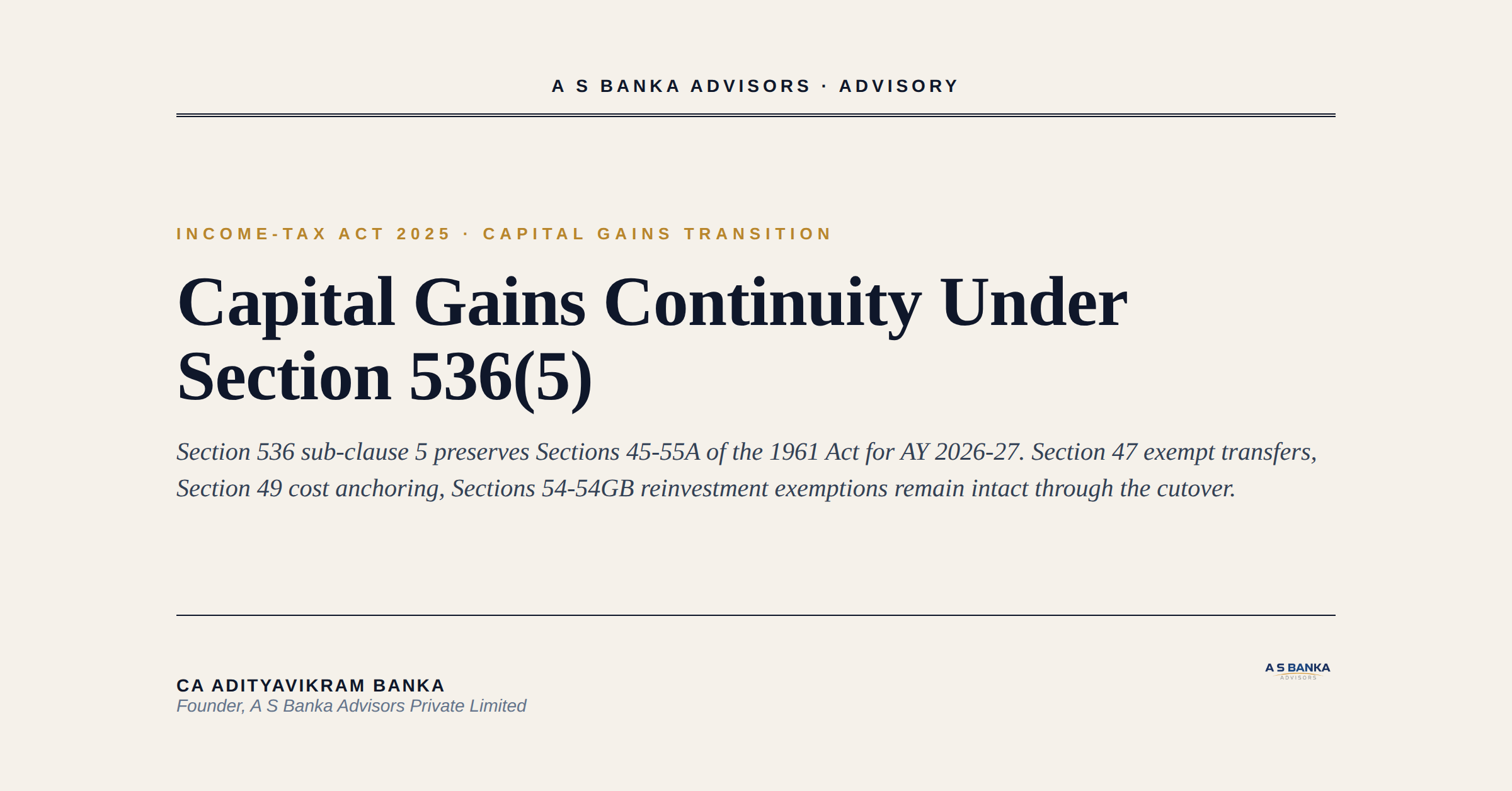

Capital Gains After April 1, 2026: Section 536(5) Keeps the 1961 Act Live for AY 2026-27 Files

The Income-tax Act 2025 takes effect from April 1, 2026,…